Updated for 2025

When you’re injured in a car accident in Texas, medical bills and lost wages can start piling up long before liability is determined. That’s where Personal Injury Protection (PIP) comes in. PIP is a unique form of “no-fault” auto insurance coverage that can provide fast financial relief for you and your passengers—regardless of who caused the crash. While optional, Texas law requires insurers to automatically include PIP in every policy unless you reject it in writing. Yet many Texans remain unsure of how it works, what it covers, and whether they should buy more than the state minimum. This guide will break it all down for you.

What Is PIP Insurance in Texas?

Personal Injury Protection (PIP) is additional auto insurance that covers your medical expenses, lost wages, and certain other costs after a crash. Unlike liability coverage, which only pays for the other party when you’re at fault, PIP is designed to protect you, your passengers, and in some cases even family members or pedestrians—without having to wait for a liability determination.

By law, Texas auto policies must include at least $2,500 of PIP coverage unless the driver signs a written waiver. Many drivers don’t realize they already have PIP included in their policy or that they can purchase higher limits, such as $5,000, $10,000, or more.

What Does PIP Cover in Texas?

PIP provides a broad range of protections that can ease financial stress immediately after an accident. Here’s what it typically covers:

- Medical Expenses: Ambulance services, ER visits, hospital stays, surgeries, physical therapy, rehabilitation, prescriptions, and even dental or optometry care.

- Lost Wages: If your injuries prevent you from working, PIP reimburses a portion of your income.

- Essential Services: Compensation for help with household tasks you can’t perform while recovering, such as cleaning, cooking, or childcare.

- Funeral Costs: In tragic cases, PIP can pay for funeral and burial expenses.

Key Features of PIP in Texas

- No-Fault Protection: Coverage applies regardless of who caused the accident, ensuring quick payouts.

- Broad Coverage: Protects you, passengers, and sometimes household members, pedestrians, or cyclists.

- Flexible Limits: Minimum coverage is $2,500, but higher limits are available and strongly recommended.

- No Subrogation: Unlike MedPay, insurers cannot demand reimbursement from your settlement if PIP already paid out.

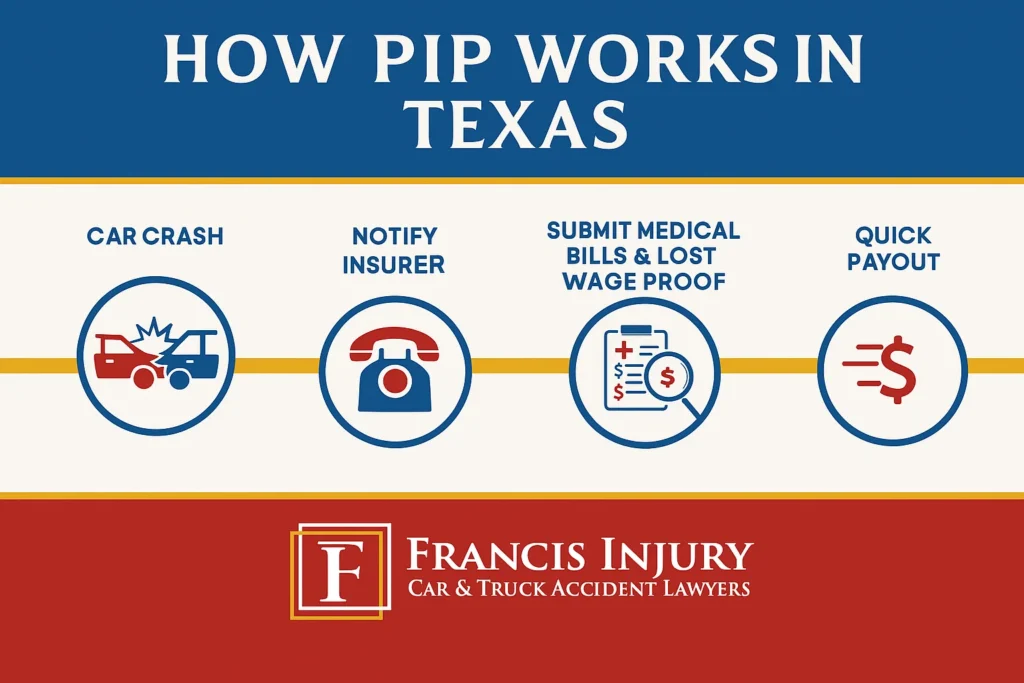

How to File a PIP Claim After an Accident

- Notify your insurer immediately after the crash.

- Gather documentation—medical bills, wage statements, and proof of out-of-pocket expenses.

- Submit your claim with supporting records.

- Cooperate fully with the insurer’s investigation to avoid delays.

PIP vs. Other Coverages in Texas

Understanding how PIP interacts with other types of insurance helps you maximize your recovery:

- PIP vs. Liability: Liability pays for others when you’re at fault. PIP covers you and your passengers, regardless of fault.

- PIP vs. Health Insurance: PIP can help cover co-pays, deductibles, and out-of-network costs before your health insurance kicks in.

- PIP vs. UM/UIM: While PIP covers immediate expenses, uninsured/underinsured motorist (UM/UIM) coverage protects you if the at-fault driver lacks adequate insurance.

- PIP vs. MedPay: MedPay only covers medical bills and can be subject to subrogation. PIP is broader and more consumer-friendly.

Should You Purchase More Than the Minimum PIP?

Most experts agree that the $2,500 state minimum is rarely enough. With rising healthcare costs, even one ambulance ride and an ER visit can exceed that amount. Many Texas drivers wisely choose $10,000 or more in PIP coverage to ensure meaningful protection. The cost increase is usually modest compared to the benefits.

Common Misconceptions About PIP in Texas

- “I don’t need PIP because I have health insurance.” Health insurance won’t reimburse lost wages or essential household services—PIP does.

- “PIP is the same as MedPay.” Not true. MedPay has fewer benefits and can reduce your settlement because of subrogation rights.

- “I waived PIP, so I can’t get it now.” You can add PIP back to your policy during renewal. It’s worth revisiting.

Texas Law on PIP: Know Your Rights

Under Texas Insurance Code §1952.151, insurers must offer PIP in every auto policy. If you didn’t sign a written rejection, you likely have it—even if you’re not aware. This is a powerful consumer protection rule in Texas law.

Real-World Example: How PIP Helps Texans

Imagine a driver in Fort Worth suffers whiplash and a knee injury in a rear-end collision. Their PIP coverage immediately pays for ER bills and two weeks of lost wages—without waiting for fault to be proven. Later, when their attorney secures a settlement against the negligent driver, PIP does not reduce that payout. This quick relief is why PIP can be a lifeline after accidents.

How Francis Injury Can Help After a Texas Car Accident

Even with PIP, insurance companies sometimes delay, deny, or underpay claims. An experienced attorney can ensure you receive full benefits and explore additional compensation options, including liability and UM/UIM claims. At Francis Injury, our Fort Worth car accident lawyers fight to protect your rights and maximize your recovery. Call us today at 817-329-9001 for a free case evaluation.

📞 Need Help After a Car Accident?

Call Francis Injury at 817-329-9001 or use our Accident Settlement Calculator to estimate your claim value today.

Our Fort Worth Office

Texas PIP Insurance FAQs

No, but insurers must include it automatically unless you reject it in writing.

The minimum is $2,500, though higher amounts can be purchased.

Yes, it covers you and your passengers, and sometimes household members or pedestrians.

No. PIP is not subject to subrogation in Texas.

Yes, funeral and burial expenses are included.

PIP covers more (lost wages, household services) and isn’t subject to subrogation.

Yes, you can add it back during policy renewal.

No, they serve different purposes and complement each other.

- Can You Sue for a Minor Car Accident in Texas?

- What Evidence Strengthens a Texas Car Accident Claim?

- The Role of Expert Witnesses in Serious Accident Cases

- Passenger Rights After a Car Accident in Texas

- Can You Wear Headphones While Driving

- Replace Your Child’s Car Seat After an Accident: A Complete Guide for Texas Parents

- Do You Need a Front License Plate in Texas? (2026 Guide)

- Is It Illegal to Drive Barefoot? The Ultimate 2026 Guide

- 2026 Guide: Penalties for Driving Without Insurance in Every State